When it comes to securing your family’s financial future, understanding the rules around life policy payouts is crucial. You might think the payout process is simple—just a matter of claiming the money after a loss.

But the truth is, there are important rules and options that can affect how and when the benefits reach you or your loved ones. Whether you’re a policyholder or a beneficiary, knowing these details can make a huge difference in how smoothly things go during a difficult time.

Ready to learn how life policy payouts really work, what to expect, and what steps you need to take? Keep reading—this guide breaks it down clearly so you can feel confident about your policy and its benefits.

Payout Methods

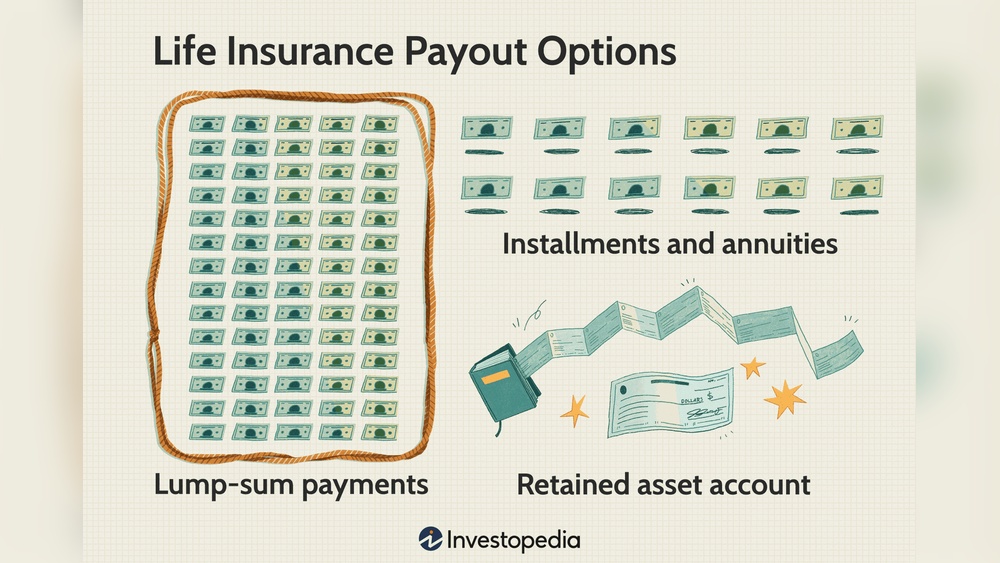

Lump Sum payouts deliver the entire amount at once. Beneficiaries get full access to the money immediately. This method is simple and fast. It helps cover urgent expenses like bills and debts.

Installment Payments spread the payout over time. The money comes in regular parts, such as monthly or yearly. This helps manage funds carefully and provides steady income. Beneficiaries avoid spending all money quickly.

Retained Asset Accounts keep the payout in an account with the insurance company. Beneficiaries can withdraw money as needed. The account may earn some interest. It offers flexibility and easy access to funds.

Annuities give regular payments for a set period or life. This option provides long-term income security. Beneficiaries receive fixed amounts to help with ongoing expenses. Annuities reduce the risk of running out of money.

Claim Process

To begin the claim process, notify the insurer as soon as possible after the policyholder’s death. Contact details are usually provided on the insurance policy documents or the insurer’s website. Prompt notification helps speed up the payout.

The insurer requires specific documents to process the claim. These often include the death certificate, the original life insurance policy, and a completed claim form. Some insurers may ask for additional papers like medical records or proof of identity.

The timeline for claim approval and payout can vary. Most companies process claims within 30 to 60 days after receiving all required documents. Delays may happen if paperwork is incomplete or if the insurer needs to investigate the claim further.

Eligibility Criteria

Beneficiary designations must be clear and up to date. The named beneficiary receives the payout directly. If no beneficiary is named, the money goes to the insured’s estate. Always review your designations after major life changes like marriage or divorce.

Disqualifying factors can stop the payout. These include non-payment of premiums, fraud, or if the insured dies during the contestability period, usually the first two years of the policy. Some policies exclude coverage for death by suicide within this period.

The policy status is crucial. The policy must be active and premiums fully paid. Lapsed or canceled policies usually do not pay out. Some policies allow a grace period for late payments, but coverage may be limited during this time.

Tax Implications

Life insurance payouts usually do not count as taxable income for beneficiaries. The death benefit is typically paid tax-free. However, interest earned on delayed payouts may be taxed as income.

Estate tax may apply if the policy owner’s estate is large. This depends on federal and state laws. The policy’s value is added to the estate if the owner has control over the policy.

Taking a loan against the policy can have tax consequences. If the loan is not repaid, it may reduce the death benefit. Unpaid loans could be treated as taxable income in some cases.

Special Situations

Payouts for chronic illness may be available under some life policies. These policies allow early access to funds if the policyholder suffers from a serious health condition. This feature helps cover medical bills or long-term care costs. The amount paid depends on the policy terms. It reduces the final death benefit.

Life insurance and disability benefits differ. Life insurance pays after death, while disability insurance provides income if the insured cannot work due to injury or illness. Some policies combine both features for better protection.

Selling your policy is an option if you no longer need it or need cash. This is called a life settlement. Buyers pay you a lump sum less than the death benefit. It requires approval from the insurer and may affect your taxes.

State Laws And Regulations

Each state has its own rules for life policy payouts. These laws affect how the money is given to beneficiaries. Some states require payouts to be lump sums, while others allow installment payments or annuities.

States also differ in how they handle disputes over payouts. Legal protections exist to ensure beneficiaries receive what they are owed. Some states have waiting periods or require specific documents before paying out.

| State | Payout Method | Legal Protections |

|---|---|---|

| Texas | Lump sum or installment | Strong beneficiary rights |

| California | Lump sum only | Strict claim documentation |

| Florida | Installments allowed | Waiting period rules |

Common Questions

Policies can sometimes be cashed out early, but it depends on the policy type. Some offer a cash value you can access before death. This value grows over time but may be less than the total premiums paid. Early cash out might include fees or penalties, reducing the amount you get.

If no beneficiary is named, the payout usually goes to the policyholder’s estate. This can cause delays as the payout must pass through probate court. Probate can take months and may reduce the payout due to court costs and fees.

| Number of Beneficiaries | How Payouts Are Handled |

|---|---|

| One | The entire payout goes to that person. |

| Multiple | Payout is split based on percentages listed in the policy. |

| No percentages listed | Payout is divided equally among all beneficiaries. |

Frequently Asked Questions

Will Life Insurance Pay Out For Cirrhosis?

Life insurance may pay out for cirrhosis if it is not excluded in the policy. Coverage depends on policy terms.

How Does A Life Insurance Policy Payout Work?

A life insurance payout goes to beneficiaries after submitting a claim and required documents. Payouts can be lump sum, installments, or annuities. The insurer processes the claim, then distributes funds based on the policy terms. Beneficiaries usually receive the money tax-free.

Does Life Insurance Cover Parkinson’s?

Life insurance may cover Parkinson’s if diagnosed after policy approval. Pre-existing conditions could affect eligibility or premiums.

What Disqualifies Life Insurance Payout?

Life insurance payouts get disqualified if the policyholder commits suicide within the contestability period. Fraud, non-disclosure, or missed premium payments also void payouts. Death due to illegal activities or policy lapses can prevent beneficiaries from receiving benefits.

Conclusion

Understanding life policy payout rules helps beneficiaries access funds smoothly. Payouts can come as lump sums, installments, or annuities. Knowing the required documents speeds up the claim process. Payout amounts depend on policy terms and conditions. Some factors may delay or reduce the payout.

Always keep your policy details updated and clear. This knowledge ensures your loved ones receive financial support when needed. Stay informed and prepared for any future claims.

Read More

- International Health Insurance Policy: Essential Benefits Explained

- Best Policy Coverage Options: Ultimate Guide for Smart Protection

- Small Business Insurance Policy: Essential Coverage for Success

- Health Policy Deductible Guide: Essential Tips to Save More

- Term Life Policy Quotes: Find Affordable Rates Fast Today

- Short Term Health Insurance Plans: Affordable Coverage Made Easy

- Whole Life Insurance Benefits: Unlock Financial Security Today

- Insurance Policy Renewal Discount: Maximize Savings Today!

- High Value Asset Insurance Policy: Protect Your Priceless Investments

- Cyber Liability Insurance Policy: Essential Protection for Your Business