Are you wondering how much a professional liability policy will cost you? Understanding the price of this important coverage can feel confusing, but getting clear on the numbers is crucial for protecting your business without breaking the bank.

Your professional liability insurance shields you from costly lawsuits and claims, so knowing what to expect in terms of cost helps you plan wisely. You’ll discover the key factors that influence your policy price and learn how to find affordable options tailored to your needs.

Keep reading to take control of your professional liability costs and safeguard your future with confidence.

Average Premiums

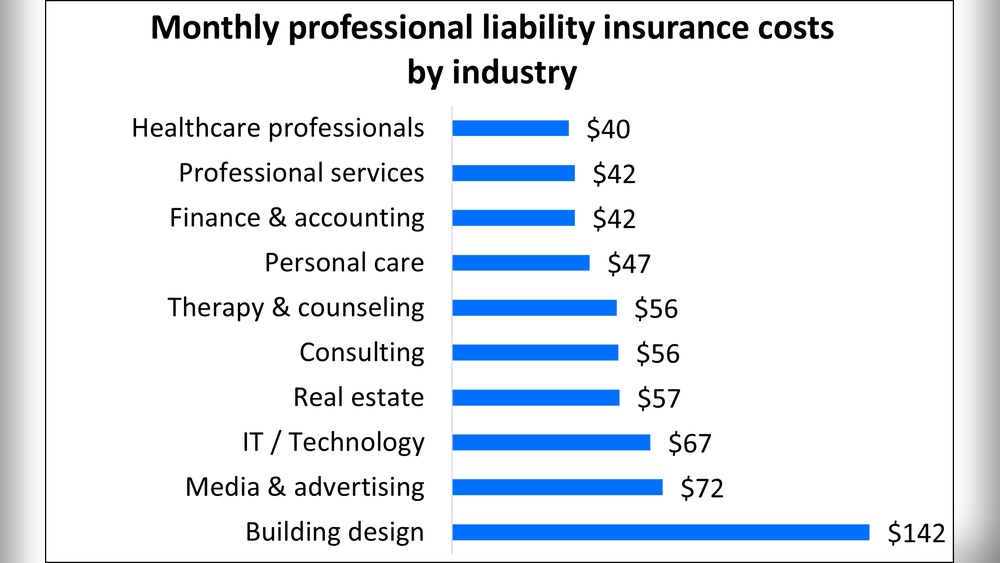

Professional liability insurance premiums vary widely by profession. For example, doctors and lawyers pay higher premiums than consultants or freelancers. Typical annual costs range from $500 to $3,000 depending on risk and coverage level.

Monthly payment options can help spread out costs but may add a small fee. Paying annually often saves money in the long run.

| Profession | Annual Cost Range |

|---|---|

| Doctors | $1,500 – $5,000 |

| Lawyers | $1,000 – $4,000 |

| Consultants | $500 – $2,000 |

| Freelancers | $400 – $1,500 |

Location also affects pricing. Urban areas tend to have higher premiums than rural ones. This is due to more claims and legal costs.

Risk Factors

Claim history plays a big role in the cost of your policy. Businesses with many past claims usually pay higher premiums. Insurers see them as riskier. A clean claim record can help lower your cost.

Different industries face different risks. For example, a tech consultant might pay less than a medical professional. This is because some fields have higher chances of lawsuits. Insurance companies use this info to set prices.

Business size and revenue also affect cost. Larger businesses or those with more income often pay more. This is because they may face bigger claims. Small businesses usually get lower rates.

Policy Details

Coverage limits define the maximum amount an insurance policy will pay. Higher limits mean better protection but cost more. Lower limits may save money but increase risk.

Deductibles are amounts you pay before insurance kicks in. Choosing a higher deductible lowers your premium. A lower deductible means you pay less out of pocket during a claim.

Many policies offer additional coverage options like cyber liability or legal expenses. Adding these can increase the cost but provide broader protection. Always balance coverage needs with budget.

:max_bytes(150000):strip_icc()/Liability-insurance_final-1c2c4bbf923b4933b62582d6d006079c.png)

Market Influences

Insurance providers offer different rates for professional liability policies. Each company has its own way of calculating risk and premiums. This leads to wide price differences even for similar coverage.

State regulations play a key role in pricing. Some states require higher minimum coverage or have special rules. These factors can raise or lower the cost of insurance. Knowing your state’s rules helps estimate expenses better.

Economic trends also affect policy costs. When the economy is weak, claims may rise, pushing prices up. Strong economies often mean fewer claims and more stable rates. Insurance companies adjust prices based on these trends to stay balanced.

Ways To Lower Premiums

Good risk management practices can lower your insurance premiums. Keeping clear records and following safety rules shows insurers you are careful. This reduces the chance of claims and helps lower costs.

Bundling policies means buying multiple insurance types from one company. This often gets you a discount. Bundling professional liability with other business insurance saves money and simplifies payments.

Shopping around helps find the best price. Different insurers offer different rates for the same coverage. Comparing quotes ensures you don’t pay more than necessary. Be sure to check coverage details, not just price.

Special Considerations

Consultants and freelancers usually pay lower premiums. Their risks are smaller because they work alone or with few clients. Costs depend on the type of work and client contracts.

Startups and small businesses may face higher costs. New companies have less history and more uncertainty. Insurance companies see them as riskier. Premiums can be higher until the business proves stability.

High-risk professions like doctors, architects, and engineers pay the most. Their work can cause big financial damage. Insurance companies charge more to cover these risks. Safety measures and experience can help reduce costs.

Frequently Asked Questions

How Much Does A $1,000,000 Liability Insurance Policy Cost?

A $1,000,000 liability insurance policy typically costs between $400 and $1,500 annually. Prices vary by industry, location, and risk factors.

How Much Should Professional Liability Cost?

Professional liability insurance typically costs between $500 and $2,000 annually. Rates depend on industry, coverage limits, and business size.

Is 200 A Month For Liability A Lot?

Paying $200 a month for liability insurance is common for many professionals. Costs vary by industry, coverage, and location. This amount is reasonable if it fits your risk level and business size. Comparing quotes helps ensure you get fair pricing for adequate protection.

How Much Is Insurance On A $10,000 Engagement Ring?

Insurance on a $10,000 engagement ring typically costs 1% to 2% of its value annually. Expect to pay $100 to $200 per year. Rates vary by provider, coverage type, and location. Getting multiple quotes helps find the best price and coverage for your ring.

Conclusion

Understanding professional liability policy cost helps protect your business wisely. Costs depend on your profession, coverage limits, and risk factors. Choosing the right policy ensures you avoid expensive legal claims. Small changes in coverage can impact your premium price. Regularly review your policy to keep it affordable and effective.

Staying informed leads to smart decisions and peace of mind. Protect your work without overspending by knowing what affects your costs.

Read More

- International Health Insurance Policy: Essential Benefits Explained

- Best Policy Coverage Options: Ultimate Guide for Smart Protection

- Small Business Insurance Policy: Essential Coverage for Success

- Health Policy Deductible Guide: Essential Tips to Save More

- Life Policy Payout Rules: Essential Insights You Need to Know

- Term Life Policy Quotes: Find Affordable Rates Fast Today

- Short Term Health Insurance Plans: Affordable Coverage Made Easy

- Whole Life Insurance Benefits: Unlock Financial Security Today

- Insurance Policy Renewal Discount: Maximize Savings Today!

- High Value Asset Insurance Policy: Protect Your Priceless Investments